Backhoe financing puts a loader and an excavator, built into a single machine, on your job site for a fixed monthly payment instead of one painful check. The backhoe loader earns its keep precisely because it does two jobs, but that dual capability still carries a serious purchase price, and the contractors who lean on backhoes hardest, utility crews, septic installers, rural builders, municipal subcontractors, rarely have that kind of cash sitting idle between jobs.

Dimension Funding has financed equipment for small and medium-sized businesses since 1978, and backhoes sit inside the same construction program that covers its dozer, excavator, and dump truck lending.

The company funds new and used backhoe loaders with a fixed rate for the entire term, monthly payments up to 60 months, and a one-page application for amounts up to $250,000. If you already know which machine you want, you can start a financing application and hear back the same day. If you are still deciding between a backhoe and a pair of compact machines, that decision is worth settling before any paperwork starts.

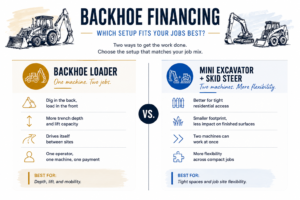

One Machine or Two: The Question Behind Every Backhoe Purchase

Most backhoe buyers today are really choosing between two configurations. The first is the classic backhoe loader, digging in the back and loading in the front. The second is a mini excavator paired with a skid steer, which splits the same work across two smaller machines. The compact pair has taken real ground on tight residential sites, where narrow gates and finished lawns punish a full-size backhoe.

The backhoe wins where depth, lift, and distance matter. Aaron Robinson, a product consultant for site development at John Deere, told Heavy Equipment Guide that sewer work usually requires a backhoe because of its lift and trench-depth requirements, while mini excavators dominate residential utility and fiber-optic trenching. A backhoe also drives itself between sites on public roads, which means no trailer, no second truck, and no second operator just to move iron.

The financing math follows the same fork. A backhoe is one contract and one payment covering both functions. The compact route means two machines, and if that is where your job mix points, Dimension Funding finances mini excavators under the same program terms. Either way, the structure of the deal should follow the work, not the other way around.

What Backhoe Financing Covers

The financing extends beyond the machine itself. Under its construction equipment financing program, Dimension Funding can finance 100 percent of the project, including delivery and maintenance costs that buyers often omit from the budget. Getting a backhoe from the seller’s yard to your first job is not free, and folding that cost into the contract means you pay almost nothing upfront.

New and used backhoes both qualify, and the used market is where the term length does its real work. A well-maintained backhoe has a long working life, and Dimension Funding structures the term around that life, up to 60 months, so the payments end while the machine is still producing. For a used unit, that alignment matters more than any single rate point, because nobody wants to keep paying for iron that has already left the fleet.

What It Takes to Qualify

Dimension Funding keeps the requirements short and publishes them plainly. Here is what the company looks for on a backhoe deal:

- At least two years in business. This is the firm requirement. Startups under two years old do not qualify for the backhoe program.

- A completed application. Approvals up to $250,000 run on a one-page application with no financial statements. Deals above $250,000 require financials.

- Credit somewhere on the spectrum. Programs are set up for everything from A+ credit to marginal credit, so a past rough patch does not automatically end the conversation.

From there, the paperwork is electronic end-to-end. Applications and contracts go through DocuSign, approvals usually come back the same day, and funds typically arrive within two to three business days. Filling out the financing application before you settle on a specific machine is a legitimate move. It costs nothing, carries no obligation, and tells you your real budget before you start negotiating with a seller.

How the Numbers Work: Terms, Payments, and Taxes

Three program features shape your monthly payment.

Term length. Financing runs up to 60 months. A longer term lowers the monthly payment, while a shorter term reduces total interest paid. A backhoe that anchors your daily work can justify an aggressive payoff. One that fills gaps between rentals may fit better on the full 60 months.

Fixed rate. The rate is locked at signing and holds for the entire term, so the payment you budget in year one is the payment you make in year five.

Deferred first payment. Qualifying borrowers can take no payments for the first 90 days, with restrictions. That window lets the backhoe start billing hours before the first payment comes due, which helps when the machine is tied to a contract that has not yet started paying.

The payment calculator on Dimension Funding’s site shows how a given purchase price spreads across different terms, and checking it before you talk to a seller beats checking it after.

There is a tax dimension as well. The Section 179 deduction allows businesses to deduct qualifying equipment in the year it goes into service rather than depreciating it over time, and IRS rules extend this to financed purchases.

A backhoe financed in the fall and put on a job before year-end may be deductible that same tax year, even though most of the payments have not been made. Your accountant should confirm eligibility, which turns on business income and the total equipment you place in service, before the deduction goes into your budget.

Buying a Used Backhoe? Check These Before You Sign

A financing approval does not include an inspection of the machine for you. Before signing on a used backhoe, verify these items yourself or pay a heavy equipment mechanic to do it:

- Swing tower and kingpin play, since slop in the swing pivot is one of the most expensive repairs a backhoe can need and easy to feel during a test dig.

- Loader arm pins and bushings, which take a beating on machines that spent their life loading trucks.

- Hydraulic cylinders and hoses for leaks, scoring, or drift when the boom holds a load.

- Hour meter readings against maintenance records, because hours tell you more than the model year does.

- Tires, since backhoes travel on pavement between sites and road miles wear rubber faster than dirt does.

- A clean title and a lien search on the serial number.

A careful inspection protects the financing decision as much as the purchase decision. Sixty months is a long time to make payments on a machine with a worn-out swing frame.

Getting a Backhoe Financed with Dimension Funding

Dimension Funding has been underwriting equipment purchases since 1978 and holds an A+ rating from the Better Business Bureau. For a backhoe deal, that history translates into a short application, an answer the same day in most cases, and money moving within two to three business days, all of it handled electronically.

When the right machine shows up, apply for financing online or call 800.755.0585 and walk through the deal with a person rather than a portal. A buyer whose financing is already moving negotiates from a stronger position than one still waiting on a bank.

Frequently Asked Questions

How long can I finance a backhoe?

Backhoe financing through Dimension Funding is available for up to 60 months, and the rate stays fixed from the first payment to the last. Terms are matched to the machine’s remaining working life, which keeps used backhoes fully eligible.

What credit score do I need to finance a backhoe?

There is no published minimum credit score for the program. Dimension Funding structures financing across the full range from A+ down to marginal credit, with two years in business as the one firm requirement. Where you fall on that range tends to shape your rate rather than your approval.

How fast can I get approved for a backhoe loan?

Approvals typically come back the same day you apply. Funding follows within two to three business days, and deals up to $250,000 skip financial statements entirely in favor of a one-page application.

Is it better to finance or lease a backhoe?

Dimension Funding offers both equipment financing agreements and equipment lease agreements, and the right structure depends on how long you plan to keep the machine. Financing suits contractors who want to own the backhoe outright at the end of the term, while equipment leasing suits operations that prefer to upgrade machines on a set cycle.

Does the financing cover delivery and other project costs?

Yes, Dimension Funding’s program can finance 100 percent of the project, which bundles delivery, maintenance, and similar costs into a single contract with the backhoe itself. Nothing about getting the machine to your site needs to be recorded in your account as a separate expense.